FESTIVE CHEER FOR SOUTH AFRICAN SMALL-CAP VALUATIONS

17/12/2020

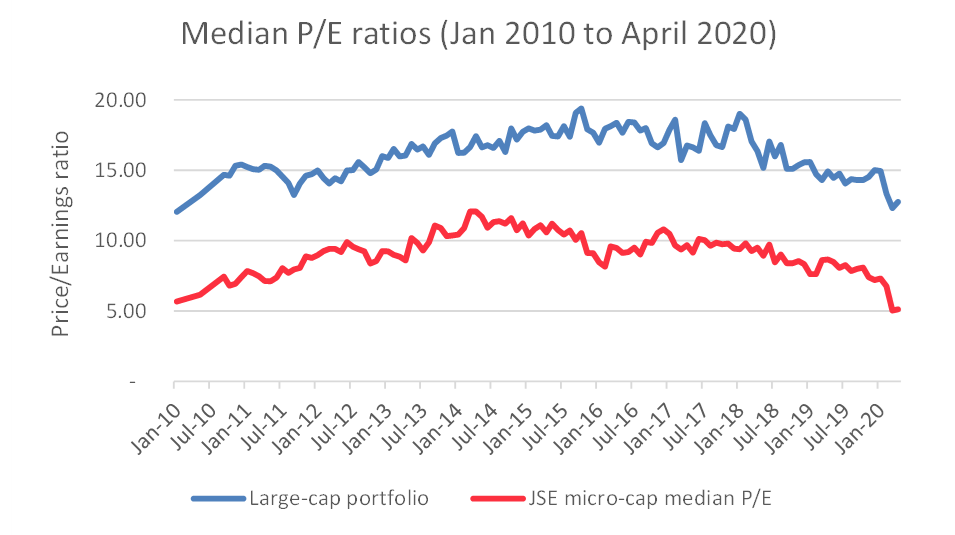

In May of this year we reported that the average Price/Earnings (“P/E”) ratio of JSE-listed, small-capitalisation companies (which provides guidance for the valuation of South African SME’s) had declined significantly in the second half of the past decade due to the weakening state of the local economy and a myriad of other challenges faced by the country.

The bad news continued in 2020 as small-cap valuation multiples were further decimated by the onset of COVID-19. This opened up a significant gap between the pricing of large and small JSE companies (“the Small Stock Discount” or “SSD”), with the average small-cap P/E ratio being 60% lower than large-cap companies. As at 31 March 2020, the median small-cap P/E ratio was a lowly 5 times earnings, representing a 10 year low.

By the close of business on Friday 4 December 2020, the JSE Allshare Index (“ALSI”) had reached a level of 59 419. This is significant as it eclipses the highest point achieved during this disastrous year, which was recorded back in January, before COVID-19 wreaked havoc on global financial markets.

Following several announcements during November of major progress in developing a vaccine to combat the pandemic, the devastation on the JSE’s leading index has been reversed, but what does this mean for the smaller constituents of the JSE, and indeed, for the pricing of South African businesses in general….

SA Incorporated recovers…. well, sort of….

Due to its significant weighting in favour of multi-national behemoths like Naspers, AB-Inbev and British-American Tobacco (which have limited local operations), the ALSI is a poor barometer for the sentiment towards, and valuations of, South African businesses. In order to assess whether the valuations of “SA Incorporated” had recovered from COVID-19, we calculated the median month-end P/E ratio of the smallest quartile of JSE-listed companies (“the Micro-cap portfolio”) and compared it to the median ratio of the upper quartile JSE-companies (“the Large-cap portfolio”).

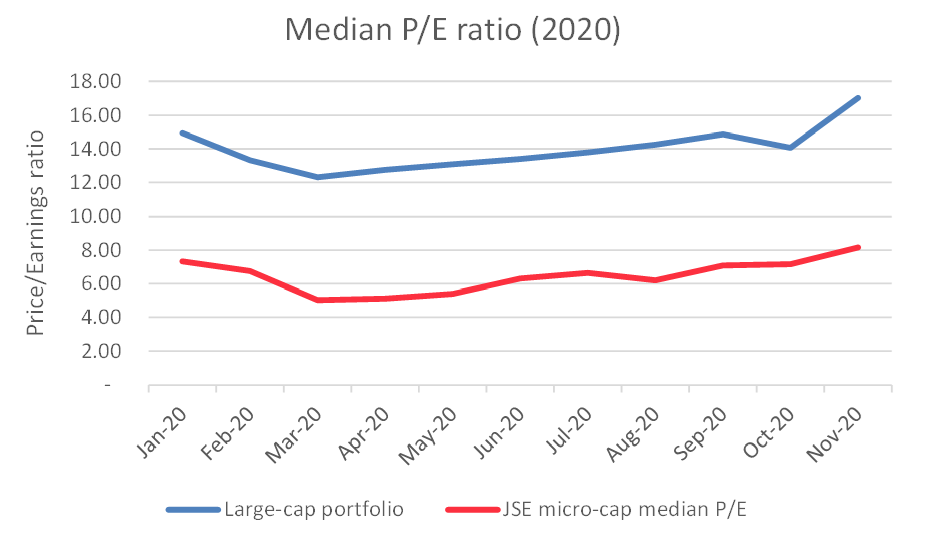

As can be seen from the chart above, the median P/E ratio of the smallest JSE-companies followed broadly the same pattern as the largest companies listed on the exchange (ie. a major decline between January and March as the magnitude of the COVID-19 threat became evident, followed by a gradual recovery of share prices and valuations between April and October.

November was an exceptionally strong month for global equity markets with the announcement of promising developments in the search for a COVID-19 vaccine. Light at the end of the tunnel spurred a recovery in large and small cap shares alike and by 30 November 2020, the median P/E ratio of the Micro-cap portfolio had increased from an embarrassing low of 5 in March to a respectable 8.2, which is not far off the two-year peak of 8.7 recorded in April 2019.

The Small Stock Discount also recovered strongly between April and October and by the end of November, the gap between the median P/E ratio of the Large-cap and Micro-cap portfolios had decreased to 52%, which is only marginally higher than the levels we are accustomed to seeing.

The natural (and appealing) conclusion from the increase in the average P/E ratio is that the valuation multiples of the JSE’s fledgling companies have recovered to pre-COVID-19 levels. The recovery of the Micro-cap portfolio’s P/E ratio between April and November, however, only tells half the story as the earnings base of the JSE companies (the denominator in the P/E ratio) has been eroded due to the effects of South Africa’s lockdown.

With financial reporting, there will always be a lag between the incurring of losses and the reporting thereof. As a result, the market prices (the “P” in the P/E ratio) adjusted as soon as the severity of the pandemic became known while the earnings (the “E” in the ratio) only adjusted once the reporting company had issued trading results which covered a portion of the lockdown period.

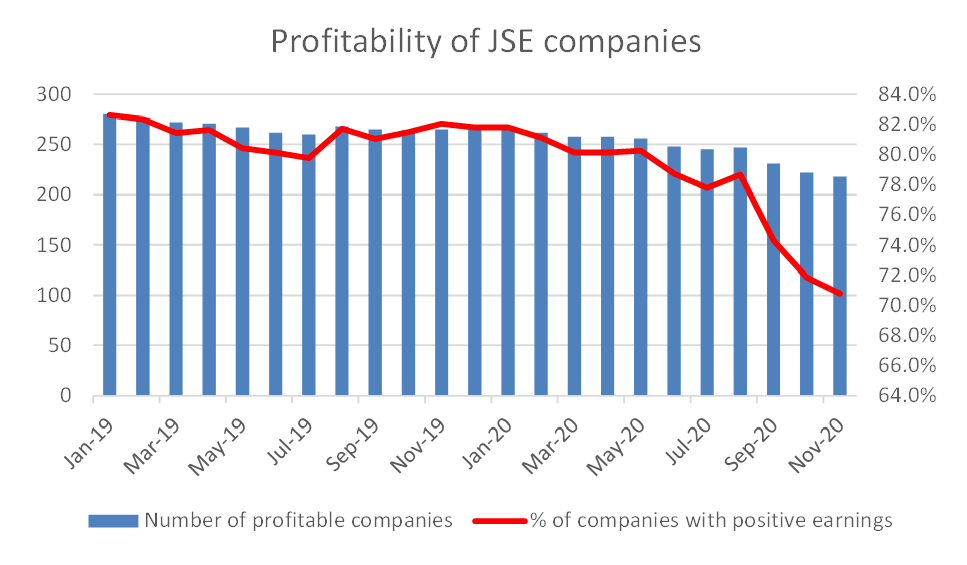

The chart below reflects the number of JSE-listed companies which reported positive earnings since the start of 2019, along with the percentage of the exchange which showed a positive P/E ratio. Prior to May 2020, more than 80% of the JSE’s constituents reported positive earnings but from May onwards, this percentage fell off the proverbial cliff as a growing number of companies reported results which were prejudiced by lockdown trading conditions.

Conclusion

The recovery in the market prices of small South African companies is certainly good news but with this much noise in the market, investors and valuers should proceed with caution when using market multiples (such as the P/E ratio) to estimate the fair value of a business. The panic-selling which drove the decline in market prices has abated, but we have many concerns relating to the current earnings base.

The reduction in business volumes caused by lockdown, coupled with the abnormal costs associated with an adjustment to the way many firms conduct business, has resulted in earnings levels which may bear no relation to the long-term, sustainable earnings of the subject business. A further, and somewhat cynical view, is that some management teams may use this disastrous year as an opportunity to clean up their balance sheets by raising provisions for losses and impairments which should have been raised in prior periods, thereby making COVID-19 the scapegoat for prior year’s mistakes.

Now, more than ever, those looking to buy or sell their business need to enlist the services of experienced valuation professionals who will go beyond the application of rule of thumb approaches to truly understand the prospects and value of their business in these unprecedented times.